Note: A version of this article about insurance premium increases appeared in our LinkedIn newsletter, Pricing Power Clarity®.

Trust Buffett, it’s a great business

It’s no wonder Warren Buffett loves the insurance business. He famously declared “The single most important decision in evaluating a business is pricing power.” That statement is getting help from insurers of all stripes to make Mr. Buffet look both the sage and the oracle.

(At EBITDA Catalyst we collect quotes about pricing. You never know when you’ll be called on to be the life of the party!)

Auto insurance and health insurance seem to have a lot in common these days, though we’ll focus mostly on auto in this article. For one, most consumers have seen significant rate increases in their policy premiums already, while the insurers have been in a chorus claiming they are hit with ever higher claims and inflation in repair and replacement costs.

Price increases across the nation seem to claim familiar “cost-plus” rationales

Consider the following recent reports, one from CA and one from MN, about insurers’ price actions and consumers’ (and watchdogs’) dwindling options to fight back.

LA Times: Californians, brace for another bill increase: your car insurance

TL;DR: The insurers want higher premiums now that drivers, after 2 years of COVID, are back on the roads at pre-COVID levels and, allegedly, the cost of covering claims is up.

Key quote:

The most common (rate increase) request is 6.9% because anything larger than that can trigger a public hearing. Some of the biggest names on the pending list include State Farm, Progressive, Farmers and the American Automobile Assn. Geico, the state’s second-largest auto insurer, after State Farm, got a 6.9% rate increase in December, which will mean a premium boost averaging $125 a year for the company’s 2.1 million policyholders.

The size of the rate increase is not “value-based”, rather it’s “what can one get without additional scrutiny”-based.

Cost-plus rationales apply … only when costs go up?

As reported in the LA Times story, the same insurers disagree with and are failing to pay back consumers for windfalls collected during COVID when next to no one was driving and claims dropped dramatically. E.g. cost-plus pricing is invoked only when costs rise, and rejected when they fall. This of course is the standard consumers should expect from inflation-driven price increases. As we have argued in our whitepaper back in early 2021, savvy industry leaders end up with more profit, not less, during and following inflation.

Take it or leave it?

Further, insurers are effectively doing with state regulators exactly what #consumerbrands are doing with retailers that try to resist price increases: they threaten to stop selling.

AP News: Insurers say California’s inaction threatens auto policies

TL;DR: Insurance companies want consumers to believe that without the profit margins they want, there won’t be insurance and we’ll all be worse off.

This particular argument sounds familiar. We’ve heard it every time pharma or health insurers, too, explain why those prices go up faster than the economy.

For regulators or Congress to stand firm in this game of chicken here in America, however, they need something they don’t have, and insurers and pharma companies do: staying power (market & economics savvy would also help, in a distant second kind of way). The upshot is clear: insurance companies leverage concentrated decision-making, communications, lobbying, and a game plan that is proactively, and expertly focused on their incentives. Consumers and the regulators or elected representatives supposed to represent them … have no such things (in America). In the systems we have set up, insurers pursue exactly the incentives we have created and do an amazing job of it. The paralyzing political division that prevents changing those incentives appears to be well on its way to a self-reinforcing market mechanism. Expect insurance companies to keep winning. And don’t blame the players, blame the game.

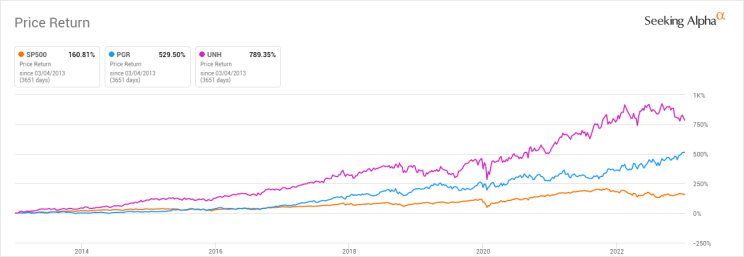

Are insurers suffering? Don’t believe rhetoric, believe the market

This 10-year chart (as of early March) tells the story of how much the “smart money” believes auto insurers like Progressive (or health insurers like United Health) are really “hurting” or expected to hurt in the future from rising costs.

Market outperformance depends on (occasionally) higher claims

During one of the better 10-year performance periods in decades for the S&P 500, Progressive has still outperformed it for with a price return over 3X that of the index. Notably, the outperformance has been even more dramatic recently, despite the “woe is us” chorus of car insurers. The market is not just failing to worry about Progressive’s profits, it appears to price in significantly better profits than at the beginning of 2022.

Are all those allegedly faster-driving and more frequently inebriated drivers returning great for Progressive and its peers, even if we accept for a moment as true that claims and costs are higher?

Of course, they are. As long as insurers can impose their rationale of cost-plus rates, costs going up means profits (and EPS) are going up, even before we factor in operating leverage from fixed costs (Progressive’s employees, buildings, etc that presumably don’t scale up linearly with claims).

It could be noted that other insurers like Allstate, State Farm or Hartford haven’t done quite as well as Progressive, while Geico is not publicly traded (owned by Buffett’s Berkshire Hathaway).

Geico and State Farm reported large losses in auto insurance businesses in 2022. Yet in their commentary, they both feel great about their business there anyway.

Why? Because having the occasional money-losing year is a great part of the whole logic of an insurance business! It’s exactly what allows for large insurance rate increases that then keep on giving for many “normal years” … increasing the pie on which the industry collects, over longer periods a healthy % of ever-rising total premiums paid.

Losses provide insurers with their best reason to exist (and pass on insurance premium increases)

More importantly, large losses provide exactly the “scare factor” that amplifies risk aversion and leads consumers to buy insurance to begin with (where they even have a choice in the matter). Insurers are well capitalized to withstand a couple of years of significant underwriting losses. Most non-outlier years result in underwriting surplus/profit. That “float” of premiums and surplus Buffett so dearly loves to invest earns handsome returns over the vast majority of years to support giant cushions from which to pay up in down years.

Berkshire predicts GEICO will generate an underwriting profit in 2023.

What is left for consumers to do?

Absent an unlikely, dramatic turn in America’s trajectory as a political and market system, insurance companies will continue to make growing profits from the market as a whole. They have perfected using both good years and bad years to fuel their long-term profits. Buffett knows it, and he’s been trying to tell us for a long time.

Some will self-insure

This is already happening for many consumers who simply can’t afford the insurance premium increases. MN KARE11 / NBC: With car insurance costs up 14%, many decide to ‘self-insure’

For anyone deciding to do this, it’s important to be smart about it. First understanding what options exist and what is “average” or “reasonable” for premiums in a given market requires work. Sites like Bankrate have useful tools. But under-insuring ourselves while continuing to over-risk is not a winning strategy.

The best consumer response: aggressively manage your risk “consumption”

Whether consumers self-insure or diligently comparison shop for rates from insurers, the same market reality applies: when premium rate increases become unaffordable, a rational response is, if at all possible, to consume less!

But it’s important to understand that in this industry, we have two inputs amounting to “consumption”:

- What risk exposure do we take on (including our own risky or unhealthy behaviours, how much we drive, where we live and park, etc)? In other words, how much risk we “consume.” In fairness, some portion of this risk is not in our control, but much of it is.

- What subset of that risk did we outsource to insurers to cover? In other words, how much insurance do we consume to mitigate our risk consumption from 1 above? Of course, some insurance is mandatory in most states if you drive. Yet expensive additional insurance, like collision and comprehensive, is not (unless your vehicle is financed and the lender requires it).

Conclusion

It is a rare industry where we consumers have a direct impact on the largest cost driver. Yet in the insurance market, consumers are simultaneously fighting the legitimacy of insurance premium increases. Managing items our insured risk “consumption” is something every consumer can do more about. Yet the evidence suggests that, collectively, we’re headed the other way. We should not expect insurance companies to reward our higher risk any differently than they always have. They will keep turning more insurable events into higher profits, underwritten by … us.

Did you enjoy this post? Stay in touch!

- Don’t forget to hit the “Subscribe” button. (100++ curious minds join our newsletter every week!)

- ???? Tap my profile bell to catch the next post that is “not” in the newsletter! Here’s how (LinkedIn cool feature I didn’t know about either until recently)

- Follow EBITDA Catalyst